Kross Retail Company is coming up with its IPO fresh issue of Rs. 250 crores and offer th for sale worth Rs. 250 crores, totalling Rs. 500 crores which will open on 9 September th 2024. The issue will close on 11 September 2024 and be listed on the exchange on th 16 September 2024. In this article, we will look at the Kross Retail IPO Review and analyze its strengths and weaknesses. Keep reading to learn about the company.

Kross Limited IPO – About the Company

The company was incorporated in 1991. Kross specializes in manufacturing trailer axles, suspension assemblies, and high-performance safety-critical parts for medium and heavy commercial vehicles and farm equipment. With over three decades of experience, they have become a prominent player in India’s trailer axle industry. The company serves a diverse client base, including large OEMs, tier-one suppliers, and domestic dealers.

The business model relies on backward integration, with in-house design, process engineering, forging, casting, and machining capabilities. This approach gives them greater control over processes, timelines, pricing, and quality. They also offer forward integration for their trailer axle business, providing sales and service locations across key states in India.

The company operates five manufacturing facilities in Jamshedpur, Jharkhand. These facilities have advanced machinery for forging, foundry work, machining, coating, and heat treatment. They have obtained various quality certifications which ensures high standards in their manufacturing.

Kross Limited IPO – About The Industry

The automotive industry in India is changing. The government’s PLI scheme aims to boost manufacturing and reduce dependence on imported parts. The scheme

focuses on high-tech green vehicles like electric and hydrogen fuel cell models. It excludes traditional petrol, diesel, and CNG vehicles. PLI offers incentives for advanced technology components and vehicle aggregates across different segments.

Tractor demand depends on farmer incomes and rural infrastructure development. Farmers use tractors for both agriculture and commercial purposes. Non-farm usage, including construction and transportation, accounts for 18-23% of tractor demand. This trend is likely to grow as farmers look for ways to make tractor ownership more economically viable.

The commercial vehicle sector shows promise. The MHCV industry may grow 2-4% annually and Bus sales increase by 1-3% from 2024 to 2029. Improved road infrastructure and higher disposable incomes will drive growth. The CV industry has already recovered well, reaching 96% of pre-pandemic levels in fiscal 2024.

Kross Limited IPO – Financial Highlights & Segments

Kross Retail reported revenue from operations of Rs. 620.25 crores in FY24, and Rs. 488.62 crores in FY23. Net Profits in FY24 stood at Rs. 44.88 crore, and Rs. 30.93 crore in FY23. The company had a magnificent jump in profits from FY22 where it posted Rs. 12.16 crore.

Most of the expenses are spent on acquiring materials which forms a major part of the expenses of around 61.05% compared to revenue. Other expenses form another huge part of expenses, including spare part consumption, Power & Fuel expenses, Labour charges, work offloading charges, and others in FY24.

PAT Margins in FY24 was 7% which is better than 6% in FY23. In FY24, the EPS was Rs. 8.30 per share and Rs. 5.72 per share in FY23. This is a significant improvement from FY22. The EPS increase is attributed to the revenue growth.

The company’s debt-to-equity ratio stood at 0.80 in FY24 compared to 0.86 in FY23. In FY23, 35.45% was the Return on Equity compared to 36.06% in FY24. The increase in ROE was due to an increase in revenue and profit margin which made a huge difference in returns.

The ROCE stood at 28.15% compared to 27.51% in FY23. The improvement in operational efficiency and revenue has helped the ratio to improve. Inventory Turnover ratio stood at 8.27 in FY24 compared to 8.88 in FY23.

Kross recognises its revenue from operations under manufacturing of critical components for M&HCV and farm equipment and most of the sales are in India. M&HCV accounts for around 88.87%, Farm Equipments accounted for 9.02% and the remaining 2.11% from Other components or services in FY24.

Kross Limited IPO-Listed Key Players

The listed peers of Kross Retail are Ramkrishna Forgings Limited, Jamna Auto Industries Limited, Automotive Axles Limited, GNA Axles Limited, and Talbros. Automotive Components Limited.

Compared to its peers, the Gross Profit Margin of Kross is around 42.62% which is in the higher range relative to its peers. The Gross Margin ranges from 28% to 49%. The PAT margins of Kross stood at 7.22% which is in the lower range of its peers. The peers ranging from 6% to 14%, Kross has underperformed among its peers.

The difference between Gross margin and profit margin is the EBITDA margin which is used to understand operational efficiency. The contrast between the two can be known from EBITDA Margin. Kross was 13.02% compared to its peers range of 11% to 21%. Kross is near the lower range of its peers.

Most of the companies in this industry have high borrowings which relates to looking at the Solvency ratio. The debt-to-equity ratio for Kross stood at 0.80 times compared to its peer’s range of 0.01 times to 0.80 times. The Kross ratio is in the higher range.

The RoE of Kross was 30.57% which is in the higher range of its peers and ROCE saw the same trend as RoE. The RoE was maintained YoY despite higher interest costs, lower equity base, and higher profits which ensured decent returns among its peers. Overall the Kross performed par in some parameters and underperformed in some with the peers.

Strengths Of The Company

- Customer Relations: The company maintains long-standing relationships with major OEMs and suppliers. They serve over 200 customers across various segments, including M&HCV and farm equipment. Their ability to customize products and consistently deliver quality solutions has strengthened these customer relationships.

2. Capacity: They are a prominent manufacturer of trailer axles and suspension assemblies in India. The company has witnessed robust growth between Fiscal 2021 and 2024, enabling it to compete with major trailer axle manufacturers. Their manufacturing capacity is 60,000 trailer axle and suspension assemblies per annum.

- Product Diversification: The company offers a diverse product portfolio, focusing on continuous value addition. They manufacture a wide range of forging and machined precision components and assemblies. Their engineering capabilities allow them to produce complex and high-precision products, including safety-critical components

for various automotive applications.

- Manufacturing Capabilities: They have integrated manufacturing operations with in-house product and process design capabilities. This integration allows greater. control over processes, timelines, pricing, and quality. Their backward integration capabilities include forging, design, casting, and machining. This improves operational efficiency which reduces the dependence on third parties.

- Leadership Experience: The company boasts experienced leadership and a strong management team. Their Chairman and Managing Director have over three decades. of experience in the automotive industry. The management team’s expertise in various fields which includes operations, product development, and others.

Weaknesses Of The Company

- Revenue linked with Automobile Demand: The company’s demand is directly linked to vehicle sales by their customers. A decline in sales of M&HCV and farm equipment can adversely affect their business. Economic conditions, regulatory changes, and industry trends might impact the demand for their products.

- Lack of Long-Term Contracts with Customers: They lack long-term contracts with customers. The company operates on a purchase-order basis, which doesn’t guarantee future business. This arrangement makes it difficult to predict demand and plan production schedules accordingly.

- Pressure on Price: The company faces pricing pressure from customers. They may need to reduce prices to retain business or increase market share. This can lead to pressure on margins and might affect their profitability and ability to increase prices in the future.

- Operational Cost Impact on Profit Margin: Profitability may be impacted by various factors which include raw material costs, finance costs, and labour costs. Revenue growth doesn’t always lead to increased profits due to volatility in profitability margins. They operate in a competitive industry with fluctuating expenses. 5. Risk in Receivables: Kross is exposed to counterparty credit risk. Delays or defaults in customer payments can adversely impact their cash flows and working capital. They may need to spend significant amounts recovering dues, which might affect their financial condition and prospects.

Kross Limited IPO – GMP

The shares of Kross Retail Ltd’s price in the grey market were trading at a 0% premium th as of September 5, 2024. The shares in Grey Market traded at Rs.240. This gives it a premium of Rs.0 per share over the cap price of Rs. 240.

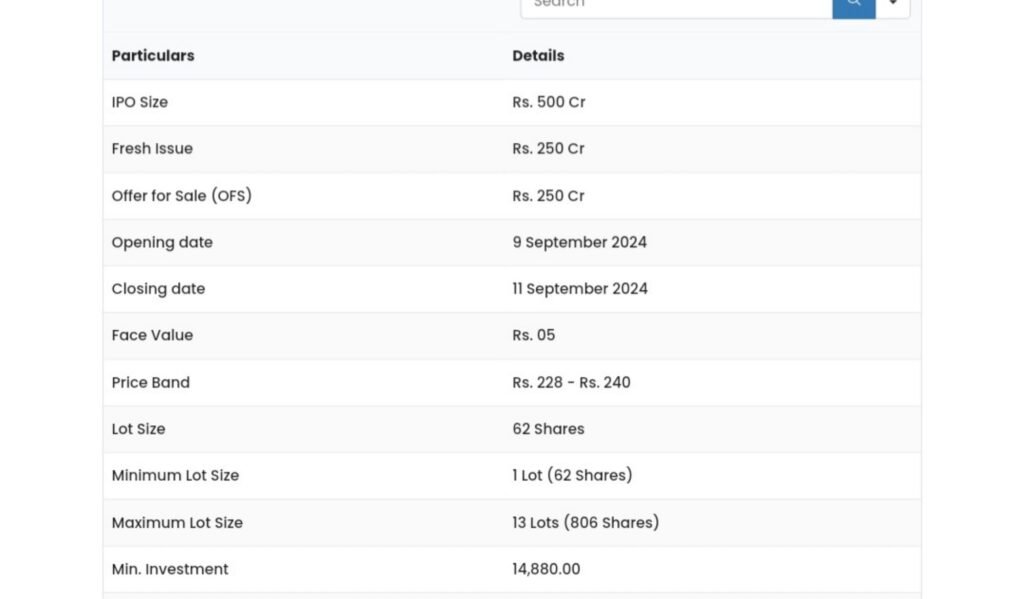

Kross Limited IPO – Key IPO Information

Promoters: Sudhir Rai, Anita Rai, Sumeet Rai, and Kunal Rai.

Book Running Lead Manager: Equirus Capital Private Limited.

Registrar to the Offer: KFin Technologies Limited.

The Objective Of The Issue

Rs. 228-Rs. 240

62 Shares

1 Lot (62 Shares)

13 Lots (806 Shares)

14,880.00

16 September 2024

- Capital expenditure funding requirement to purchase machinery and equipment – Rs. 70 crore.

- Prepayment or repayment of outstanding borrowings availed by the company – Rs. 90 crore.

- Working Capital Requirements – Rs. 30 crore.

- General Corporate purposes.

Conclusion

Kross Retail Limited is one of the players in the Auto Ancillary segment in the Automobile Industry. They have good backward integration to streamline the process to minimise the cost and improve in-house capabilities.

However, being in this sector is prone to Automobile cyclical changes which might affect their profitability margin. Being Competitive in this space needs a better understanding of the market and Management is at the forefront of the company. Reducing Debt and working capital improvements can also help the company to improve its financials as well.

So what do you think of this company? Will it be able to increase its market presence and maintain growth based on its competition with peers? What is your view? Let us know in the comments below.

Next post :- Tolins Tyres IPO – GMP, Financials And More