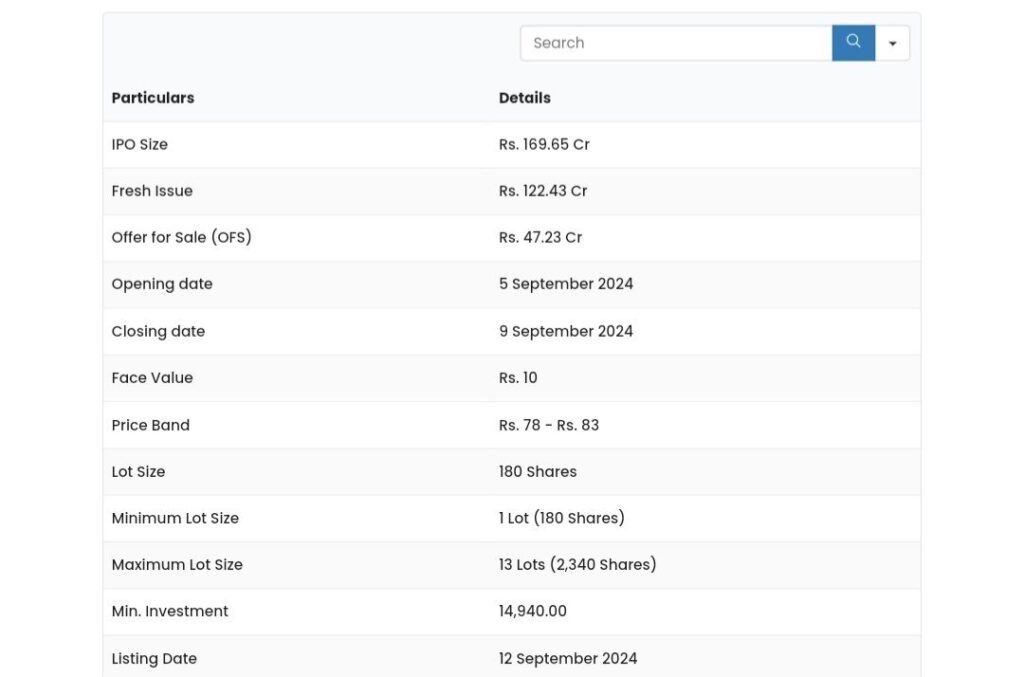

Shree Tirupati Balajee Company is coming up with its IPO fresh issue of Rs. 122.43 crores and offer for sale worth Rs. 47.23 crores, totalling Rs. 169.65 crores. which will open on 5th September 2024. The issue will close on 9th September 2024 and be listed on the exchange on 12th September 2024. In this article, we will look at the Shree Tirupati Balajee IPO Review and analyze its strengths and weaknesses. Keep reading to learn about the company.

Shree Tirupati Balajee IPO – About The Company

The company was incorporated in 2001. Shree Tirupati Balajee Agro Trading Company Limited manufactures and sells flexible intermediate bulk containers (FIBCs) and other industrial packaging products. The company operates through five manufacturing units and several subsidiaries. They offer a wide range of customized packaging solutions for diverse industries like chemicals, food, mining, and agriculture.

The company’s core competencies include a broad product portfolio, multi-location facilities, and technical expertise. It focuses on sustainability by using recycled materials and operating solar power plants for captive consumption. The company has a global customer base and has been designated as a Three Star Export House by the Indian government.

Shree Tirupati Balajee sources raw materials primarily from domestic suppliers, with some imports from international markets. The company is led by a professional management team and has over 20 years of experience in the industry. It emphasizes quality control and holds various certifications for its manufacturing processes and products.

FIBC contributes around 51.47%, Woven Sacks – 4.51%, Woven Fabrics, Narrow Fabric – 21.32%, Tape – 4.21%, and the remaining 18.49% from others as a revenue percentage in FY23.

Shree Tirupati Balajee IPO – About The Industry

The FIBC (Flexible Intermediate Bulk Container) industry in India is experiencing significant growth. Chemicals, food products, construction materials, and agriculture are the main sectors driving demand. The industry grew by 38% in the last decade, with production reaching 151.1 million units in 2024. The market value hit $926 million in 2023, growing at a 6.7% CAGR from 2020 to 2023.

India’s low labour costs make it an attractive manufacturing hub for FIBCs. This advantage has led to increased production capacity to meet global demands. The shift from high-cost regions like Turkey, Europe, and the US to India is fueling industry growth. The abundance of skilled workers at competitive wages helps keep production costs down.

The outlook for the FIBC industry in India is positive. Consumption is expected to reach 69 million units by the end of 2024, growing at a 5% CAGR from 2020 to 2023. Key factors driving growth include rising demand from chemicals, food, agriculture, and construction sectors. Government initiatives like ‘Make in India’ are also supporting the industry’s expansion.

Shree Tirupati Balajee IPO – Financial Highlights & Segments

Shree Tirupati Balajee reported revenue from operations of Rs. 539.66 crores in FY24, and Rs. 475.43 crores in FY23. Net Profits in FY24 stood at Rs. 36.07 crore, and Rs. 20.71 crore in FY23. The majority of the revenue goes into spending on material costs, employee benefit expenses, and other expenses involved in operations.

PAT Margins in FY24 were 8.79% compared to 5.70% in FY23. In FY24, the EPS was Rs. 5.74 per share and Rs. 3.51 per share in FY23. This is an improvement compared to YoY by 63.53%. The increase in EPS has benefitted the shareholders.

The company’s debt-to-equity ratio stood at 1.41 in FY24 compared to 2.03 in FY23. RoE was 25% in FY24 compared to 20% in FY23. Their increase in RoE was due to an increase in profits.

The RoCE stood at 29.14% compared to 22.33% in FY23. The revenue increase and control of freight outward costs have helped the operational efficiency ratio to improve.

Shree Tirupati Balajee recognises its revenue from operations under the manufacturing business of HDPE/PP Woven sacks fabric. Domestic Sales account for 50.96% (incl. other operating revenues) and the remaining 49.04% is from Export sales in FY24.

The majority of their revenues in Domestic markets come from the West accounting for 93.81%, North and South accounting for 2.85% and 2.23% respectively and the East accounting for 1.11% in FY24.

Shree Tirupati Balajee IPO – Listed Key Players

The listed peers of Shree Tirupati Balajee are Commercial Syn Bags Limited, Emmbi Industries Limited, and Rishi Techtex Limited.

Compared to its peers, the revenue size of Balajee’s is relatively higher than its peers. The PAT margins of Balajee are 8.79%, as compared to its peers range of 1.20% to 2.63%. The Balajee’s margin has outperformed its peers in PAT Margins.

The EBITDA margin of Balajee is around 13.58% in FY24 when compared to its peers Commercial’s and Emmbi’s of around 9%. Balajee has better returns than its peers which showcases its operational efficiency.

The RoE of Balajee stood at 25% in FY24 as compared to 5.85% of Emmbi’s, 5.66% of Commercial, and 4.23% of Rishi’s. When compared to RoCE Balajee’s stood at 29.14% which is far superior Overall Balajee has outperformed in most of the parameters among its peers.

Strengths Of The Company

1.Diverse customer base: The company serves clients across various industries, maintaining long-term relationships and securing repeat business. They offer customized FIBCs, helping customers improve performance and reduce costs, which leads to customer retention and price advantages.

2.Cost-effective products: The company’s FIBCs offer efficient load handling, ease of use, and chemical resistance. These bags reduce packaging weight and transportation costs, making them a popular choice in industries like food & beverage, chemicals, pharmaceuticals, and construction.

3.Multi-product portfolio: The company manufactures a wide range of FIBC bags for various products including food, chemicals, and mining materials. This diverse product range allows customers to source most of their packaging needs from a single vendor which ensures to maintain quality.

4.Integrated manufacturing facilities: The company operates five strategically located manufacturing facilities in Indore, Madhya Pradesh. These facilities have good connectivity to ports and highways, enabling timely and cost-effective product delivery to clients.Quality standards and certifications: The company emphasizes quality production, conducting comprehensive inspections at each stage. They hold various certifications including ISO 9001:2015, ISO 22000:2018, and BRCGS and GFSI for food-grade production, ensuring their products meet global standards.

Weaknesses Of The Company

1.Geographic concentration: All five manufacturing facilities are located in Pithampur, Madhya Pradesh. This concentration might expose the company to regional risks like social unrest, or political instability, which could impact business operations and financial conditions.

2.Dependence on plastic: The company’s products primarily use plastic as a raw material. Increasing environmental concerns and potential bans on plastic products in India or export markets could affect their business and operations.

3.Negative cash flows: The company has experienced negative cash flows from operating activities in recent years. There is an increase in borrowings in financing activities. This could impact their growth and business if the trend continues, and affecting their ability to fund operations.

4.Regional sales concentration: A majority of domestic sales come from the western zone of India. This dependence on one region makes the company vulnerable to adverse developments in that market, potentially affecting its overall business performance.

5.Raw material price volatility: The company’s primary raw materials, polypropylene and polyethylene, are subject to price fluctuations linked to crude oil prices. These fluctuations might impact manufacturing costs and profit margins, especially during events like pandemics or conflicts.

Shree Tirupati Balajee IPO – GMP

The shares of Shree Tirupati Balajee Ltd’s price in the grey market were trading at a 9.64% premium as of September 3rd, 2024. The shares in Grey Market traded at Rs.91. This gives it a premium of Rs.8 per share over the cap price of Rs. 83.

Shree Tirupati Balajee IPO – Key IPO Information

The Objective Of The Issue

1.Prepayment or repayment of outstanding borrowings availed by the company – Rs. 31.45 crore.

2.Prepayment or repayment of outstanding borrowings taken by the subsidiaries HPPL, STBFL, and JPPL – Rs. 20.82 crore.

3.Working capital fund requirements for the company – Rs. 13.50 crore.

4.Fund for Working capital requirements for its Subsidiaries – Rs. 10.74 crore.

5.General Corporate purposes.

Conclusion

Shree Tirupati Balajee has half of its revenues from domestic and exports. Most of their business is concentrated in West India. The company procures most of its materials from limited sources might pose a problem for the company if its contract expires. Their business catering to different industries is linked to the performance of those industries. Now, the business looks better as demand from customers across industries increases it looks promising.

So what do you think of this company? Will it be able to increase its market presence and maintain growth based on its competition with peers? What is your view? Let us know in the comments below.

Next post :- Awfis Space Solutions PAT expected to grow at 92% CAGR; Should you buy?